CPP Post-Retirement Benefit Explained – After retirement, people often assume that their income will become limited and that their future life will depend solely on savings or a pension. However, for seniors living in Canada, this is not entirely true. If an individual continues to work even after retiring, they have an excellent opportunity to boost their monthly income through a benefit known as the CPP Post-Retirement Benefit (PRB). This program not only encourages individuals to remain active in the workforce but also strengthens their future financial security.

What is the PRB, and how does it work?

The PRB is an additional monthly benefit available to individuals who are already receiving a Canada Pension Plan (CPP) or Quebec Pension Plan (QPP) retirement pension while simultaneously working. When you work and CPP contributions are deducted from your earnings, a new PRB—calculated based on those contributions—begins to be paid to you starting the following January. A key feature of this program is that each year’s contribution generates a new PRB; collectively, these individual PRBs accumulate over time to gradually increase your total monthly pension amount.

What are the eligibility requirements?

To qualify for the PRB, certain conditions must be met. You must be between the ages of 60 and 70. You must be employed and actively making contributions to the CPP. Additionally, you must already be receiving a retirement pension from either the CPP or the QPP. It is important to note that once you reach the age of 70, CPP contributions automatically cease, and it is no longer possible to make contributions toward the PRB thereafter.

Contribution Rules for Ages 60 to 65

If you are between the ages of 60 and 65 and are currently working, making contributions to the CPP is mandatory. This means that contributions will be deducted from your salary as well as made on your behalf by your employer. These very contributions serve as the foundation for your future PRB, ultimately leading to an increase in your pension income.

What options are available between the ages of 65 and 70?

After the age of 65, you have the option to choose whether or not to contribute to the CPP. You may continue contributing if you wish, or you may choose to stop. To discontinue contributions, you must complete Form CPT30 and submit it to both your employer and the Canada Revenue Agency (CRA). However, you may only change this decision once per year. If you are self-employed, you are responsible for paying both the employee and employer portions of the contribution yourself.

Important Information for Employers

If an employee is between the ages of 60 and 65 and is working while receiving a pension, both the employer and the employee are required to contribute to the CPP. Conversely, for employees aged 65 to 70, the employee may choose to stop contributing; however, Form CPT30 is mandatory for this purpose. It is the employer’s responsibility to implement this change immediately and to notify the CRA accordingly.

How Much Benefit Can You Receive?

The amount of the PRB depends entirely on your income and your CPP contributions. Each year of contribution generates a new PRB. The maximum benefit can amount to up to 2.5% of your CPP pension. For instance, if you contribute up to the maximum income limit, you could receive an additional benefit of approximately $49.39 per month in 2025. If your income is lower, your PRB will be reduced proportionally.

The Impact of PRB on Other Benefits

While the PRB increases your total monthly income, it may also affect other government programs—such as Old Age Security (OAS), the Guaranteed Income Supplement (GIS), or various provincial benefit plans. If your total income rises, the benefit amounts you receive from these programs—or your eligibility for them—may change. Therefore, it is essential to understand this aspect as well.

Contribution Rates

For the PRB, the CPP contribution rate remains the same as the standard CPP rate. Both employees and employers are required to contribute 4.95%, whereas self-employed individuals must contribute 9.9%. This contribution is based on your pensionable income.

Let’s Understand with an Example

Suppose a woman named Jane is receiving a CPP pension at the age of 65 while simultaneously earning $57,000 annually. If she continues to work and contribute until the age of 70, her PRB will increase each year. At age 66, she would receive an additional benefit of $337.15; at age 67, this would rise to $371.99; and by the time she reaches age 70, her annual PRB could amount to $2,042.72. If she lives until the age of 87, she could receive a total additional benefit of over $40,000.

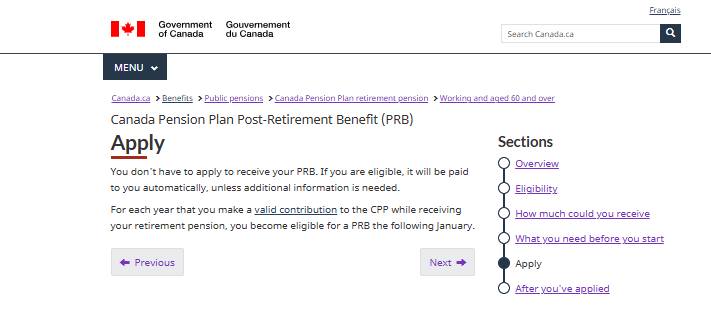

How to Apply for the PRB?

The best feature of the PRB is that it does not require a separate application. If you are working and contributing to the CPP, this benefit is automatically added to your account. A new PRB amount is incorporated into your pension starting every January. You simply need to ensure that your contributions are being remitted correctly.

Conclusion

The CPP Post-Retirement Benefit (PRB) presents an excellent opportunity for those who wish to continue working even after retirement. This program not only helps you maintain your current income but also adds a new increment to your pension each year. In today’s times—when financial security is of paramount importance—the PRB is a measure that can make your future even more secure and robust.

FAQs

Q. What is the CPP Post-Retirement Benefit (PRB)?

A. PRB is an additional lifetime monthly benefit for people who work while receiving a CPP or QPP retirement pension.

Q. Who is eligible for PRB?

A. Anyone aged 60 to 70 who is working, contributing to CPP, and already receiving a retirement pension.

Q. Do I need to apply for PRB?

A. No, PRB is automatically added if you are contributing to CPP while working.